Since the European Payment Services Directive 2 (PSD2) put in place in 2018, bank customers (individuals and businesses) can authorize a third party to use their financial data and manage their finances. How has Open Banking evolved since its launch in Europe and Belgium, and what are its perspectives of evolution?

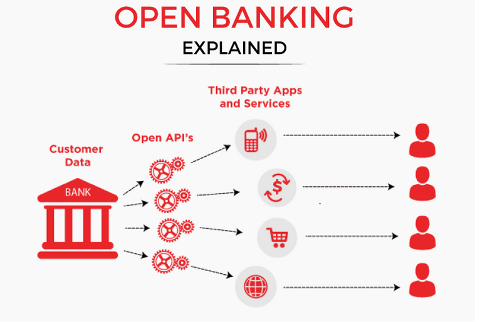

With the consent of their customers, banks are now bound to share their banking data related to payments with external companies and to allow third-party applications to initiate payments on behalf of their customers. Open Banking is the connectivity and orchestration of data between financial institutions and third-party providers to deliver new products and services to the market. This connectivity is possible thanks to Application Programming Interfaces (APIs), softwares that allow two applications to interact with each other.

In Open Banking, Third-Party Providers (TPPs) are intermediaries who help improve the interactions between bank users and their banks. They provide an interface designed to match customers’ needs and that allows them to access their financial data more efficiently. For example, TPPs can aggregate the financial data from all of the bank accounts of a consumer and display it in one interface. In other words, open banking third-party providers are licensed and registered digital service providers that act as middlemen in the banking industry.1

Figure 1 below explains the link between financial institutions, API, TPP, and consumers that constitute Open Banking.

Figure 1: Open Banking Explained – www.cashdash.in

As an example, Amazon is the Third Party Provider when a consumer orders a product on their interface. When the consumer clicks on “pay the order”, Amazon accesses their bank account and can debit the client through an API. Thus Open Banking opens the door for non-financial institutions to compete against banks in payment transactions and other financial services.

Open Banking is considered a substantial opportunity for banks to improve their customer experience. The technology allows them to provide new services or products to their customers (personalized investment advice, creation of financial reports to help them manage their bank accounts, etc.). It also helps banks in reducing their internal costs by automatizing and digitalizing processes in place (i.e.: KYC processes, onboarding processes of new clients, or credit scoring algorithms).

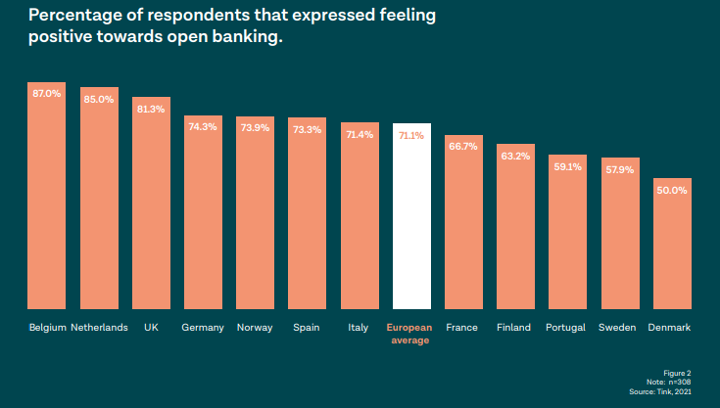

Open Banking is becoming increasingly popular amongst high-profile financial services executives, as per the survey conducted by Tink (Figure 3) and answered by 290 respondents spread around 12 European countries. According to the study, 61% of respondents are more enthusiastic about Open Banking compared to the year 2019.

Open Banking in Europe

In Europe, the implementation of Open Banking in the business strategy of financial institutions is different depending on the country.

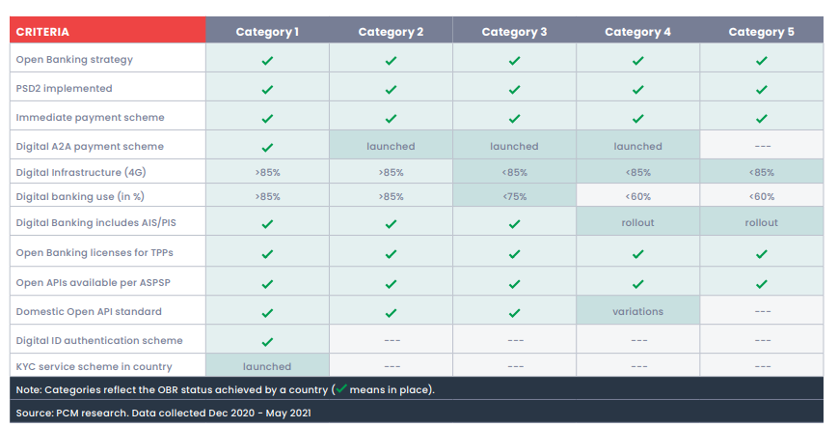

Mastercard has recently conducted a study called “Open Banking Readiness Index”[1] (Figure 2), classifying 10 European countries according to their level of Open Banking Readiness:

- Category 1: Sweden, Denmark, and Norway

- Category 2: The United Kingdom

- Category 3: France, Germany, and Spain

- Category 4: Italy and Poland

- Category 5: Hungary

Figure 2: Open Banking Readiness 2021 – 2021 Mastercard International Incorporated.

According to the study, Nordic countries are the most developed in terms of Open Banking. They have their own Domestic Digital A2A (Account 2 Account) Payments[2], like the mobile application Vipps in Norway or Mobile Pay in Denmark. Mobile Pay for example was used by 81% of the Danish population in 2019 and is the most used application before Facebook in the country. Digital A2A Payments is still at an early stage in the other country categories, as these countries have a lower digital infrastructure for 4G and the use of digital banking is lower compared to Nordic countries.

Nordic countries have also created their cross-border payment structure called P27 in 2017, which participates in making them European leaders in Open Banking. P27 brings together the largest Nordics banks and aims to build the world’s first real-time, cross-border payment system in multiple currencies[3].

Their influence is also reflected by other features like the establishment of a common pan-Nordic KYC infrastructure. Created in 2019, the company Invidem allows the centralization of bank customers’ data in a single platform making KYC processes easier and compliant with AML regulation[4]. At the moment, they are the only European countries that own a common platform.

The UK is also considered a leader in Open Banking and is estimated to lead mainland Europe by five years. This is because the country quickly put Open Banking initiatives in place. Indeed, after the Subprime crisis in 2007-2008, the national regulator FCA (Financial Conduct Authority) already supported the established Fintechs.[5] In 2018, one of the UK’s primary banks, Barclays, was also one of the first banks to provide their customers with the possibility to view all of their current and savings accounts including those from other banks in their mobile application. Transfer payments were additionally made possible from any account. This service called multi-banking was created thanks to their innovation hub of over 40 Fintechs.

What is Belgium’s vision of Open Banking?

As we can see in Figure 3 from the survey conducted by Tink, Belgium’s bank executives are the most positive in Europe about open banking, with over 87% seeing it as a positive development.[6]

Figure 3: Attitudes towards the open banking movement by country – The open banking revolution, Tink 2021

KBC was the first Belgian bank to enter the race, by integrating multi-banking in their mobile app. In 2018, BNP Paribas Fortis signed a partnership with Tink, the European leader in Open Banking platforms, providing solutions to enhance customer experiences and offer better financial products. After integrating multi-banking into their app, they aim at offering more Personal Finance Management tools (PFM) that will allow customers to have a complete picture of their financial health and receive tailored advice to better manage their money.

Open Banking has also allowed Belgian banks to develop other income streams by providing extra services such as digital partnerships with telecom companies. For example, Belfius and Proximus launched a new service called Beats in 2021. Beats offer a monthly subscription allowing to combine a banking component (accounts, cards, and insurance) and a telecom component (Internet, telephone, TV, and mobile subscription), all in a tailor-made offer based on the situation and the preferences of every customer. Through this new offer, Beats can provide an exclusive Telecom-Banking package at a very competitive price.

The limits of Open Banking in Belgium

Although PSD2 has made it mandatory for banks to share their customer data with non-financial institutions, the latter must provide a license granted by The National Bank of Belgium (NDD) along with the customers’ agreements. This additional requirement makes it more time-consuming and complex for fintechs to use the data as they please, thus fintechs consider that Open Banking in Belgium is still “mainly theoretical”[7]. Some banks also try to get around the agreement by claiming a lack of security and still refuse to share their customer data with third-party providers.

Another problematic facet of PSD2 is the fact that the regulation does not include any recommendations regarding technical aspects. This results in Banks using their own APIs, which sometimes are not compatible with Third Party Providers’ APIs. For example, Belgian Fintechs have complained about authentication procedures: as each bank has its own client identification feature (login/password, digital signature, SMS, etc.), FinTechs have had to build specific APIs for each bank, which is both costly and time-consuming.[8]

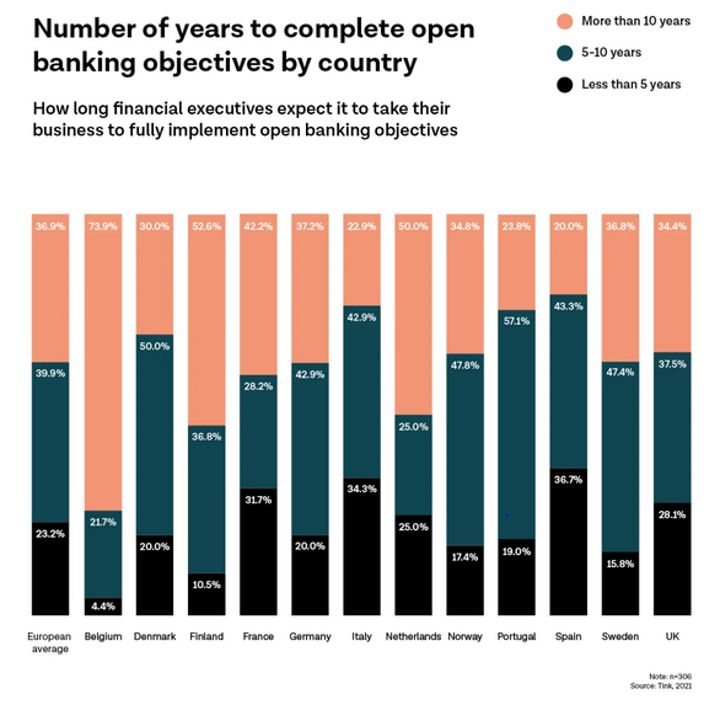

Furthermore, according to Bernard Nicolay (Professor at Solvay Business School of Economics and Management), although Belgian banks (especially the largest ones) see Open Banking as a real opportunity, they are still quite cautious about the subject. Indeed, as per another survey from Tink, 73,9 % (see Figure 4) of Belgian financial executives expect their institutions to take over a decade to complete their open banking objectives, which is the highest percentage compared to other European countries.

Figure 4: European financial institutions say it may take over a decade to complete open banking objectives – Tink, September 2021

What is the future of Open Banking in Belgium?

Open banking is one of the main drivers of digital banking transformation in the strategy of financial institutions for the year 2022.[9] Belgium is in line with this trend as the main Belgian Banks, in collaboration with Fintechs, have already started providing services such as digital payments, multi-banking, etc.

However, compared to other European countries, this enthusiasm for digitalization comes with some concerns. Belgian regulators need to review their directives to leave more room for third-party providers, for example by standardizing technical aspects amongst financial institutions. Jean-Louis Van Houwe, chairman of Fintech Belgium, has also suggested creating a new authority for Open Banking aiming to ensure a real partnership between Banks and Fintechs. This is already the case in the UK, through the organization called the Open Banking Implementation Entity (OBIE) which aims at implementing software standards and industry guidelines to drive competition, innovation, and transparency in UK retail banking.[10] and transparency in UK retail banking.

Bibliography

[1] Open Banking Readiness Index: The Future Of Open Banking In Europe A 2021 Report – ©2021 Mastercard International Incorporated – 2021

[2] Digital Account 2 Account Payments represent payments via QR code, online payments and money transfer applications.

[3] https://nordicpayments.eu/

[4] Invidem – Trust in Information

[5]Partelya Consulting done by Andréa Toucinho, Directrice Études, Prospective et Formations – june 2021

[6] The Open Banking revolution – Tink – 2021

[7] “Open banking is in België nog theorie” Jean-Louis Van Houwe, Fintech Belgium” – https://fdmagazine.be, 10th September 2021

[8] “Pour grandir, la fintech belge veut une réglementation simplifiée”, Olivier Samois – www.lecho.be, September 2021

[9] “Six Retail Banking Technology Trends for 2022” – https://thefinancialbrand.com – Jim Marous – 22nd November 2021

[10] https://www.openbanking.org.uk/

Other sources

“The uses cases and opportunities, Open banking 2020” – Tink – 2020

“Open banking : quelle structuration du Marché des paiements” – Study Partelya Consulting done by Andréa Toucinho – June 2021

“Pour grandir, la fintech belge veut une réglementation simplifiée” – www.lecho.be – 9th September 2021

“Open banking/open finance: a revolution that impacts households and businesses” – www.fintechbelgium.be – 9th September 2021

“La bataille de l’open banking ne fait que commencer” – www.lecho.be – 6th June 2018

“Belfius et Proximus lancent Beats, une offre sur mesure combinant des services bancaires et télécoms” – www.proximus.com – 11th October 2021

“BNP Paribas Fortis and Tink announce partnership” – www.bnpparibasfortis.com – 9th March 2018

“Why open banking APIs are so different” – https://www.finextra.com/ – Dmitrii Barbasura – 28th April 2021

“ The future of Open Banking in Europe ; Open Banking Readiness Index” – ©2021 Mastercard International Incorporated – 2021