The UK Financial Conduct Authority (FCA) regulator, announced on March 5th 2021, that it will no longer compel banks to submit to LIBOR after the end of 2021.

The IBORs Interest rate benchmarks such as the London Interbank Offered Rate (LIBOR), the Euro Interbank Offered Rate (EURIBOR), the Euro Overnight Index Average (EONIA), and certain other Interbank Offered Rates (IBORs) are being reformed.

LIBOR is published in five currencies (Euro, Japanese Yen, Pound Sterling, Swiss Franc, and US Dollar) and for seven maturities (overnight (spot next (S/N)), one week, one month, two months, three months, six months, and 12 months).

Certain currencies also use specific benchmarks such as EURIBOR and EONIA for EUR, the Tokyo Interbank Offered Rate (TIBOR) for JPY, the Hong Kong Interbank Offered Rate (HIBOR) for Hong Kong Dollar, and the Singapore Interbank Offered Rate (SIBOR) for Singapore Dollar.

1. Issue with LIBOR

A few years ago, we heard about the LIBOR Scandal: in 2012, an international investigation revealed the manipulation of interbank lending rates (LIBOR) by multiple banks since 2003. This manipulation is made by traders in order to increase their profits. As a result, the UK government began considering making reforms to LIBOR. In July 2017, the FCA announced that, after 2021, it will no longer compel panel banks to make submissions to calculate the LIBOR.

In July 2018, the Financial Conduct Authority (FCA) recommended, to the market participants, transition to alternative risk-free rates (RFR) which is a benchmark rate based on overnight deposit rates.

2. The IBORs transition to RFRs

Regulatory authorities, public and private sectors in several jurisdictions, including the International Swaps and Derivatives Association (ISDA), the Sterling Risk-Free Rates Working Group, the Working Group on Euro Risk-Free Rates, and the Alternative Reference Rates Committee (ARRC), have been discussing alternative benchmark rates to replace the IBORs.

In 2014, the Financial Stability Board (FSB) made a proposition to reform major interest rate benchmarks, mentioned above, and to use the risk-free rates (RFRs) which are based on overnight lending market rates.

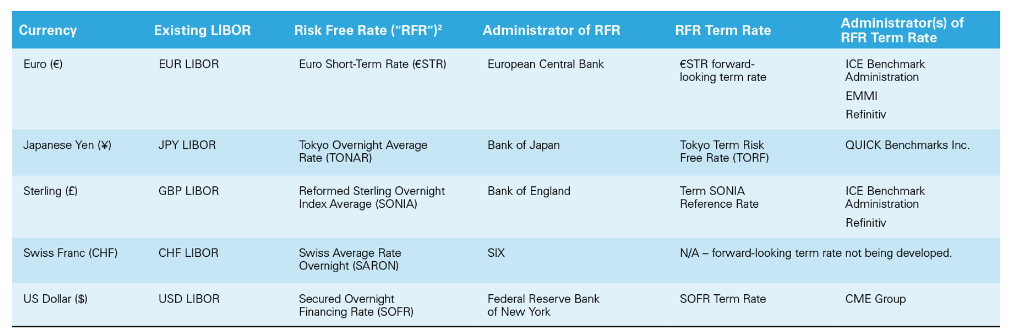

Tab: RFR Term Rates by currency

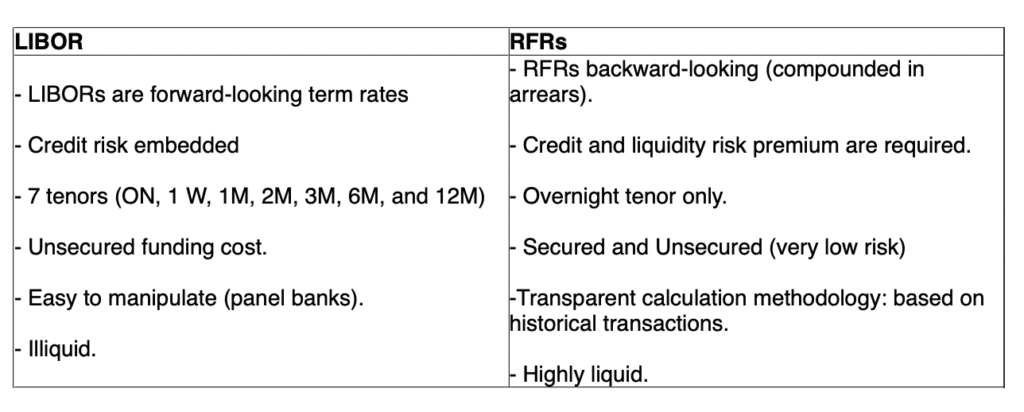

3. LIBOR vs RFRs

Find below the major differences between the LIBOR or any IBOR in general and the risk-free rate (RFRs) across major currencies. We note that RFRs are not completely risk-free, hence they are considered near risk-free. RFRs can rise or fall as a result of changing economic conditions and central bank policy decisions.

4. The ISDA’s IBOR Fallback

One question comes to mind : What happens to contracts and derivatives linked to LIBOR when this benchmark rate no longer exists?

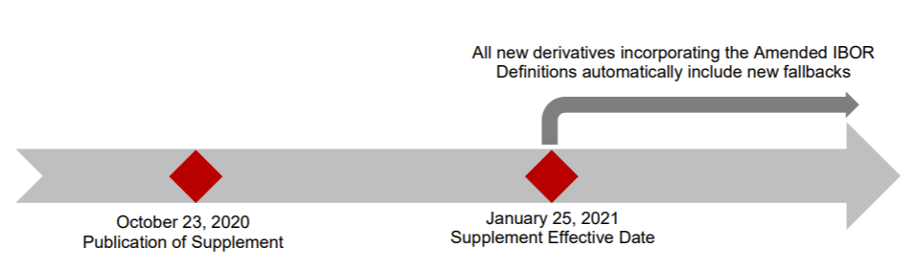

This is one of the challenging questions that was asked by professionals and the banking system. On October 23rd, 2020, the International Swaps and Derivatives Association (ISDA) has published its official Fallback Protocoland provided a response to this problem. This Fallback protocol concerns the derivatives trades that reference LIBOR or other IBORs benchmarks.

Hence, benchmark rates will “fall back” to a new benchmark in contracts that are governed by Master ISDA agreements, and the market participants will have a clear calculation and transparency of what the replacement rate would be when LIBOR is no longer available.

A party wishing to adhere to the protocol will need to sign and upload an adherence letter to the ISDA Protocol site.

Fig: The ISDA’s IBOR Fallback

But, in practice, what are the fallback rates exactly?

In fact, the relevant IBORs will first fall back to a term-adjusted risk-free rate for the relevant currency plus a spread adjustment.

IBOR = Term adjusted RFR + Spread

The term adjusted rate: for an IBOR, will be the relevant risk-free rate (RFR) for that IBOR compounded in arrears over an accrual period corresponding to the tenor of the IBOR (e.g. 1, 3, 6 months).

The spread adjustment: will be the historic median difference between the relevant IBOR and the risk-free rate over a five-year lookback period.

For example, in Europe for the transition from EONIA to €STR (€uro Short- Term Rate), EONIA usage should be restricted and its administrator EMMI announced that it will stop publishing it on January 3rd, 2022.

Since October 2nd, 2019, the current EONIA methodology has been modified to become €STR plus a fixed spread of 8.5 basis points. This spread is based on a simple average of the EONIA (pre-€STR spread between 17 April 2018 and 16 April 2019, with a 15 % trimming mechanism).

EONIA RECALIBRATED = €STR + 8,5 bp (T+1)

5. IBOR and OTC Derivatives Pricing

Let’s see how the LIBOR transition impact derivatives valuations and curve construction.

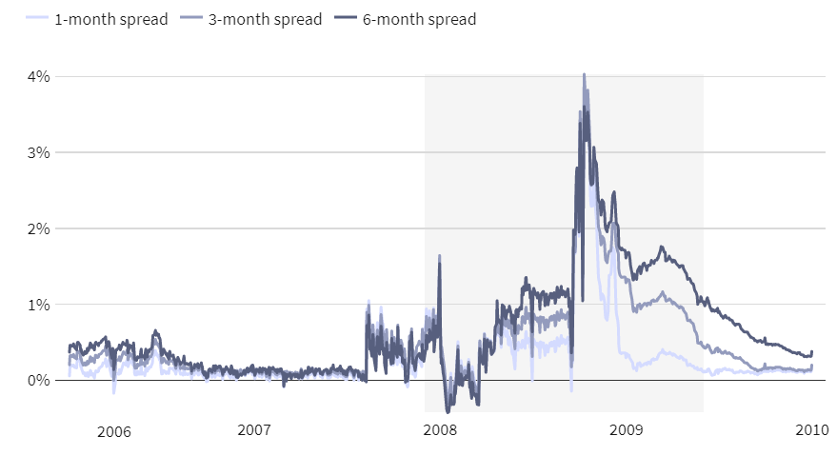

In fact, before the financial crisis in 2008, LIBOR and LIBOR-swap rates have been used as proxies for risk-free rates when valuing derivatives (i.e. fully collateralized trades were discounted at LIBOR).

However, post-2008, many banks used the overnight indexed swap (OIS) rates as the risk-free ratewhen valuating collateralized portfolios; LIBOR should be used for this purpose when portfolios are not collateralized. This means that OIS (Overnight Index Swap) remained stable under stressed conditions, and it could be adopted as the risk-free rate rather than the LIBOR.

Before the subprime mortgage crisis (2007-2008), the spread between the two rates (LIBOR vs OIS) was as little as 0.01 percentage points. At the height of the crisis, the gap reached as high as 3.65 %.

Note that an Overnight Index Swap (OIS) is an interest rate swap agreement where a fixed rate is swapped against a pre-determined published index of a daily overnight reference rate for example SONIA (GBP) or EONIA (EUR) for an agreed period.

Fig: LIBOR-OIS spread: 2006{2010 – (source: Investopedia)

Therefore, multiple pricing curves for discounting (OIS) and forecasting (LIBOR) are used, i.e., one curve (OIS) is used for discounting and multiple LIBOR forecasting curves are used for different LIBOR tenors (3-month,6-month, etc.)

As LIBOR and OIS were used in the derivatives valuation previously, replacing the OIS discounting with the RFR discounting requires a robust RFR curve.

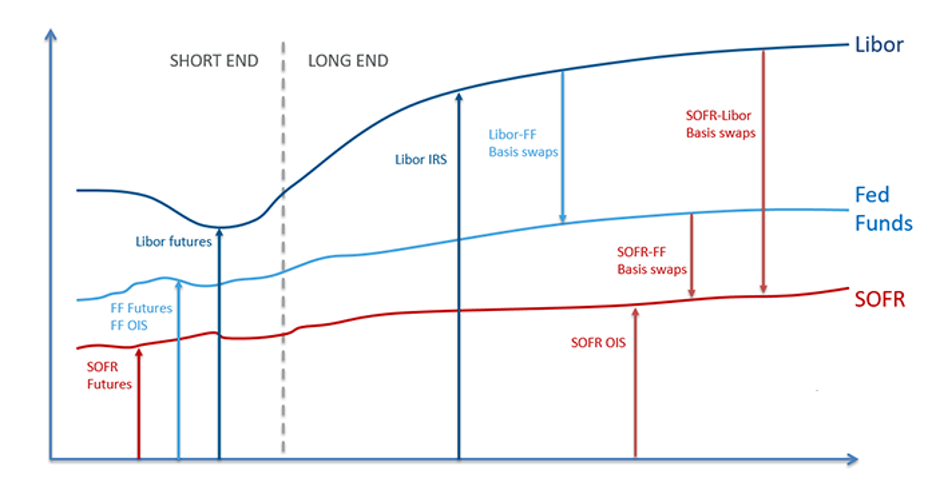

Fig: Connecting the SOFR Curve to SOFR Swaps – (Source: FINCAD)

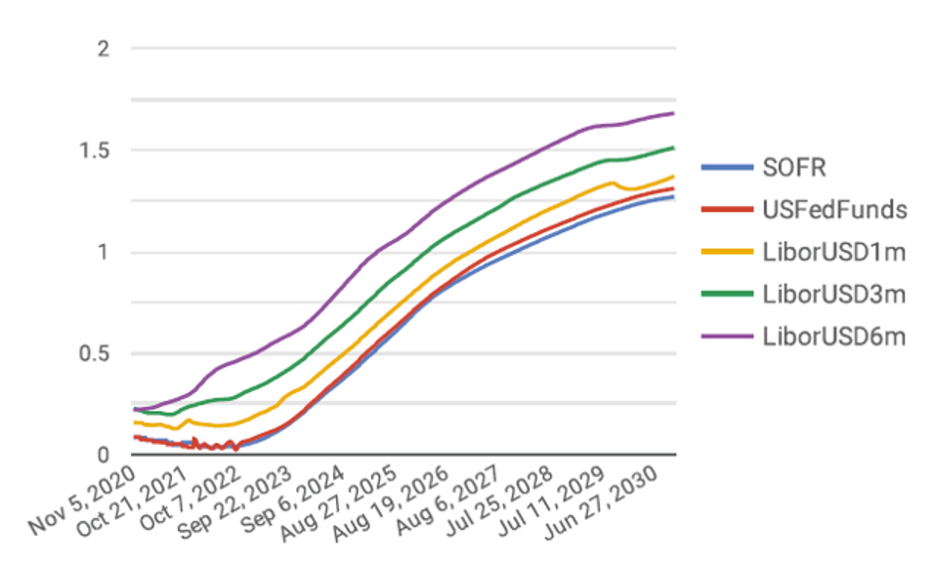

Fig: USD forward rate curves (Source: FINCAD)

Finally, RFRs are alternatives to IBOR for most market products. We see that this IBOR’s transition could have a real impact on derivatives pricing. The RFRs are based on transactions in a market with high volumes and diversity, therefore, they can bring more transparency for clients, banks, and regulators.

* Glossary :

IBOR: interbank offered rate.

LIBOR: London Interbank Offered Rate.

OIS: overnight index swap.

EFFR: effective federal funds rate.

RFR: alternative nearly risk-free reference rate.

€STR: Euro Short-Term Rate.

SONIA: Sterling Overnight Index Average.

SOFR: Secured Overnight Financing Rate.

SARON: Swiss Average Rate Overnight.

TONA: Tokyo Overnight Average Rate.

Bps: basis points, i.e., units of 0.01 %